As the lenders offer personal loans without any collateral, the risk that they bear is really high. Therefore, the lenders usually check for your credit score before approving your loan application as this indicates your credit behavior. Hence, a credit score plays an important role when getting a personal loan.

This article will help you understand what a credit score is and the different types of credit scores.

Credit Score

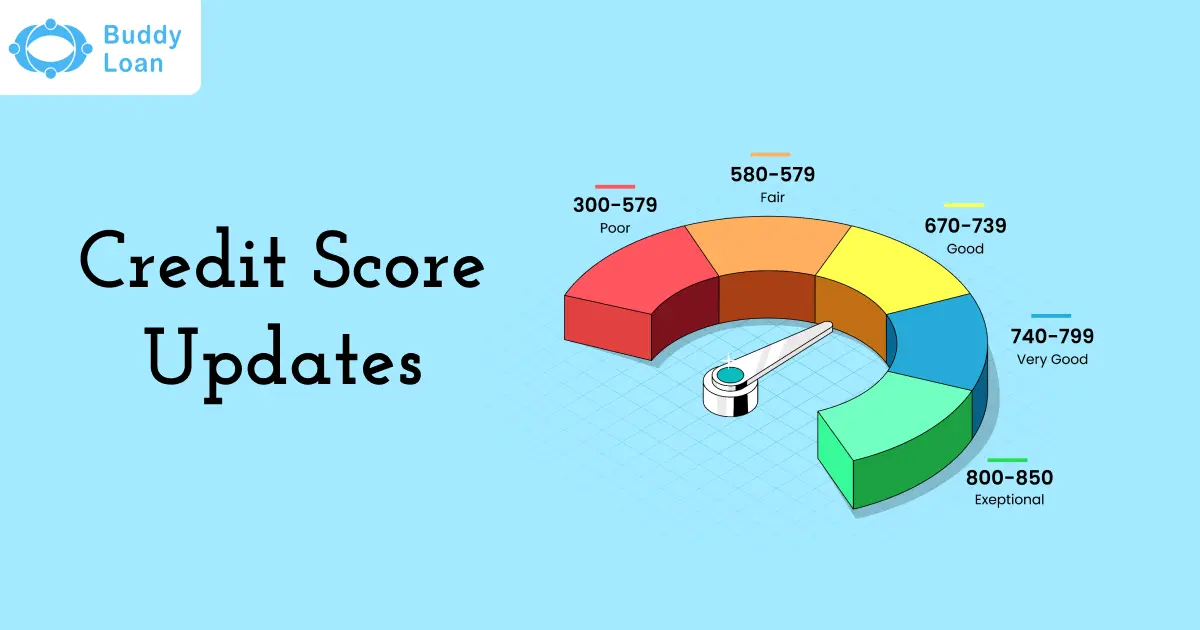

A credit score is a 3-digit number that indicates your creditworthiness. It ranges from 300 to 900 (900 being the highest and 300 being the lowest). If you have a credit score above 750, it shows that you have a good credit history and can repay your debts on time. As a result, you have a high chance of getting your loan at comparatively lower interest rates. Lenders may charge you high-interest rates if you have a poor credit score. If you want to know your credit score, you can use Buddy Score to get your full credit report instantly.

The Reserve Bank of India (RBI) has licensed four credit information companies called credit bureaus. The credit bureaus collect, collate, and aggregate the information related to an individual’s credit history and creditworthiness. They are:

- CIBIL (TransUnion Credit Information Bureau (India) Limited)

- CRIF Highmark

- Experian

- Equifax

Also Read: 10 Essential Habits for a High Credit Score

Types of Credit Score

There are two types of credit score models that banks and NBFIs frequently use:

- FICO Score

- Vantage Score

These credit score models measure an individual’s financial stability and repayment history. Here is the overview of each one in detail.

FICO Score

Fair Isaac Corporation developed the FICO score in 1989. 90% of the lenders use the FICO score while making any lending decisions. The three-digit score ranges from 300 to 850. Having a good credit score above 750 can help you avail of a personal loan at lower interest rates.

The Following Table Shows The Range And The Credit Rating Used by FICO:

| FICO Scores | Credit Ratings |

| 781 to 850 | Excellent |

| 661 to 780 | Good |

| 601 to 660 | Fair |

| 500 to 600 | Poor |

| 300 to 499 | Very Poor |

The Following Table Shows How FICO Calculates Your Credit Score

| Percentage (%) | Credit Factors |

| 35 percent | Payment history |

| 30 percent | Amounts owed |

| 15 percent | Length of credit history |

| 10 percent | Credit mix |

| 10 percent | New credit |

Also Read: Want to Achieve a Good CIBIL Score? Here are some practical tips

Vantage Score

The Vantage Score model was developed in collaboration with the three major credit bureaus (i.e. Equifax, Experian and TransUnion) in 2006. It was created as an alternative to the FICO score model.

The updated version of the Vantage Score (3.0 and 4.0) has the same range as that of the FICO score (300 to 850). Although Vantage Score and FICO score model emphasis on payment history, the Vantage Score gives importance’s to other factors such as the credit card balance and credit utilization ratio.

The Following Table Shows The Range And The Credit Rating Used by Vantage Score:

| Vantage Scores | Credit Ratings |

| 781 to 850 | Excellent |

| 661 to 780 | Good |

| 601 to 660 | Fair |

| 500 to 600 | Poor |

| 300 to 499 | Very Poor |

The Following Table Shows How Vantage Score Calculates Your Credit Score

| Influence | Credit Factors |

| Extremely influential | Total credit usage, balance and available credit |

| Highly influential | Credit mix and experience |

| Moderately influential | Payment history |

| Less influential | Age of credit history |

| Less influential | New accounts |

Personal Loan

Quick Approval in 24 Hours

💰 No processing fee for first 100 customers | ⚡ Digital KYC in 5 minutes

Factors that Impact Your Credit Score

Here Are a Few Common Factors That Affect Your Credit Score:

Payment History:

It is considered an essential part of your credit score and accounts for 35% of your FICO score. If you fail to pay your dues on time, it will reduce your credit score. Moreover, lenders check your payment history to ensure that you will repay your debts on time when approving your loan application.

Credit utilization ratio:

The credit utilization ratio is the ratio of the amount payable divided by your credit limit. If you use your credit beyond the maximum limit, your credit score will reduce. As a result, lenders will doubt your ability to repay your debts on time. Hence, keep your credit utilization below 30% of your income.

The number of Credit inquiries:

Making multiple credit inquiries will harm your credit score. Because each time you inquire, the lender does multiple background checks creating an impression that you might not repay your dues on time. It accounts for 10% of your FICO score.

Length of credit history:

Lenders check your credit history to know your credit behavior. If you have a long and positive credit history, your credit score will also be high. It also accounts for 15% of your FICO score.

Credit mix:

Having a diverse credit mix, such as student loans, car loans, credit cards, etc., increases your credit score. It indicates how well you can manage a variety of credits. It accounts for 10% of your FICO score.

Also Read : How Can Your Actions Impact Your Credit Score?

Personal Loan

Quick Approval in 24 Hours

💰 No processing fee for first 100 customers | ⚡ Digital KYC in 5 minutes

Actions That Reduce Your Credit Score

The Following Are The Typical Actions That Reduce Your Credit Score:

- Missing out on your payments: Missing out on payments or late payments can negatively affect your credit score.

- Using too much of your credit: Utilizing your credit beyond 30% reduces your credit score.

- Defaulting on accounts: Foreclosing your account, bankruptcy, settled accounts, etc., can severely hurt your credit score.

Also Read: How To Get A Credit Card Without CIBIL Score?

Tips to Improve Your Credit Score

Even if you have qualified for all the requirements, having a bad credit score can lag you behind when applying for a medical loan. So, here are a few ways you can improve your credit score to leverage your creditworthiness.

- Pay your dues on time: Have a habit of paying your dues on time, or you can set reminders to pay the bills before the stipulated deadline.

- Clear your past debts: If you have not cleared your past dues, start settling them first to increase your credit score.

- Review your credit report: Check your credit report once a year so that if there are any errors, you can clear it on time. You can check your credit report within a few minutes using buddy score

- Maintaining a good credit card balance: Keep your credit card balance below your credit limit. Hence, try not to exceed your credit utilization beyond 40%.

- Keep your old accounts open: Keep your old credit accounts open, as this will help in increasing your credit score.

Also Read : A Detailed Guide On The Crucial Tips And Tricks To Improve Your Credit Score!!

Summing Up

A credit score plays an important role when applying for a personal loan, and having a good credit score will increase getting a loan at comparatively lower interest rates. However, it would be best to keep in mind several factors that can easily affect your creditworthiness. Hence, regularly checking your credit report once a year is essential. You can also get your credit report instantly using buddy score to know your creditworthiness.

Download Personal Loan App

Get a loan instantly! Best Personal Loan App for your needs!!

Looking for an instant loan? Buddy Loan helps you get an instant loan from the best verified lenders. Download the Buddy Loan App from the Play Store or App Store and apply for a loan now!

Download the Buddy Loan app now!

Get the free Buddy Loan app on your phone

Having any queries? Do reach us at info@buddyloan.com

People Also Ask

Q. What do credit bureaus do?

A. The credit bureaus collect, collate, and aggregate information regarding your credit history and an individual’s repayment history.

Q. Does taking many personal loans affect my credit score?

A. When you take multiple personal loans, you might fail or miss out on payments, reducing your credit score.

Q. Where can I check my credit score instantly?

A. You can check your credit score instantly using buddy score to know your creditworthiness.

Q. How can I easily improve my credit score?

A. Make payments on time, review your credit report regularly once a year and avoid multiple enquiries.