Your CIBIL report is a detailed record of your credit history and financial behavior, reflecting how you manage loans, credit cards, and other forms of credit. Lenders use this report to assess your creditworthiness before approving loans or credit cards.

Reading and understanding your CIBIL report is crucial for maintaining a healthy financial profile. It helps you:

- Monitor your CIBIL score and its impact on loan approvals.

- Identify inaccuracies or discrepancies that could harm your credit rating.

- Take corrective actions to improve your financial health.

This blog will guide you through the key components of a CIBIL report, how to interpret them, and steps to ensure your report reflects your financial behavior accurately.

Sections of a CIBIL Report – What to Look For

1. Credit Score

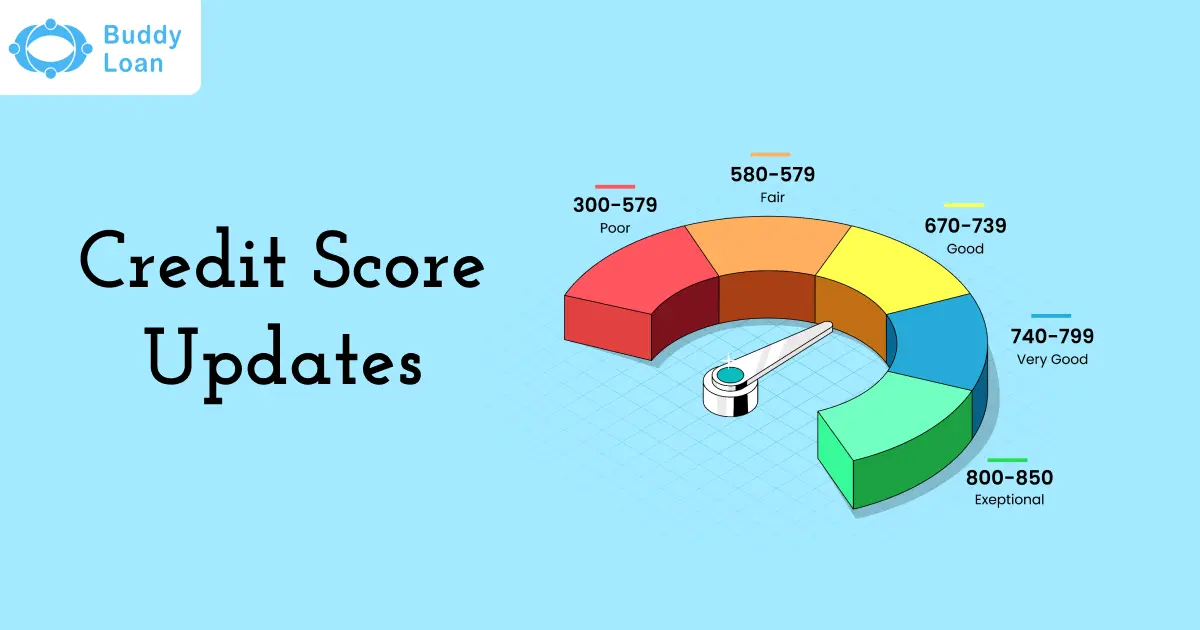

Your CIBIL score, a three-digit number ranging from 300 to 900, is at the top of your CIBIL report.

| CIBIL Score Range | Meaning | Impact |

| 750-900 | Excellent | Easy loan approvals, best interest rates, and credit terms. |

| 650-749 | Good | They are likely to get loans but at slightly higher interest rates. |

| 550-649 | Fair | Limited loan options with high interest rates. |

| Below 550 | Poor | A high rejection rate; indicates financial risk. |

At the top of your CIBIL report is your CIBIL score, a three-digit number ranging from 300 to 900” with “Your CIBIL score, a three-digit number ranging from 300 to 900, is at the top of your CIBIL report

Abbreviations:

- NA (Not Applicable): No credit history available.

- NH (No History): No active credit activity in the past 36 months.

2. Personal Information

This section includes your name, date of birth, PAN card details, and other identifiers.

What to Check:

- Ensure your name and DOB match official records.

- PAN card details should be accurate to avoid discrepancies.

3. Contact Information

CIBIL reports include up to four addresses and email IDs associated with your credit accounts.

What to Check:

- Verify the accuracy of all listed addresses (residential, permanent, and official).

- Ensure email IDs are updated, as lenders may use them for correspondence.

4. Employment Information

This section provides details of your occupation, employer name, and income (as reported by lenders).

What to Check:

- Confirm that the income and employment details match your actual records.

5. Account Information

This section is the most critical section, which summarises all active and closed credit accounts, including loans and credit cards.

Details Included:

- Account type (personal loan, credit card, etc.).

- Payment history, outstanding balances, and credit limits.

- Status codes like STD (Standard), SUB (Sub-Standard), or LSS (Loss).

What to Check:

- Look for inaccuracies in payment history or outstanding balances.

- Ensure closed accounts are marked correctly.

6. Enquiry Information

This section lists all lender inquiries made when you applied for credit.

Impact:

- Multiple inquiries in a short period can negatively affect your credit score.

What to Check:

- Verify that all inquiries are legitimate and recent.

Personal Loan

Quick Approval in 24 Hours

💰 No processing fee for first 100 customers | ⚡ Digital KYC in 5 minutes

Steps to Read a CIBIL Report – Step-by-Step Guide

Interpreting your CIBIL report effectively can help you understand your financial health and take corrective actions where necessary. Follow these steps to read and analyze your report:

1: Download Your CIBIL Report

Where to Access:

1. Official CIBIL website.

2. Trusted platforms like Paisabazaar or Cred offer free CIBIL report downloads.

Also Read: Steps to Check Your CIBIL Score on Paisabazaar

How to Download:

1. Log in to your account on the chosen platform.

2. Enter personal details like your PAN card and date of birth.

3. Verify using an OTP sent to your registered mobile number.

4. Access and download your report in PDF format.

2: Start with Your CIBIL Score

Locate your CIBIL score at the top of the report.

Understand its range and implication:

- 750 and above: Excellent creditworthiness.

- Below 650: Requires improvement.

3: Verify Personal and Contact Details

- Ensure your name, date of birth, and PAN details are accurate.

- Check listed addresses and email IDs for correctness, as lenders rely on these for correspondence.

4: Analyze Account Information

This section contains the most detailed and crucial information:

- Loan and Credit Card Details:

Verify repayment history, outstanding balances, and credit limits.

- Payment History:

- Look for discrepancies in Days Past Due (DPD) values.

- Terms like STD (Standard) indicate timely payments, while SUB (Sub-Standard) signals delayed payments.

Closed Accounts:

Ensure all closed accounts are marked as such to avoid unnecessary impact on your score.

5: Review the Enquiry Section

Check for recent credit inquiries by lenders.

Understand the impact:

- Excessive inquiries signal credit-seeking behavior, which can lower your score.

Look for unauthorized or duplicate inquiries and raise disputes if needed.

0

Bad

Check your Credit Score for Free

Your credit score is updated monthly and gives you insight into your creditworthiness. Take control of your financial future today.

Common Mistakes to Avoid When Reading Your CIBIL Report

When reviewing your CIBIL report, these common mistakes can lead to misinterpretation or missed opportunities to improve your credit score:

1. Ignoring Errors in Personal Details

- Mistakes in your name, PAN number, or date of birth can cause confusion or delays in loan processing.

- Always verify these details for accuracy.

2. Overlooking Discrepancies in Account Information

- Unrecorded payments or incorrect balances can harm your credit score.

- Cross-check repayment records and account statuses.

3. Misinterpreting Payment Status Codes

Terms like STD, SUB, and LSS have specific meanings:

- STD (Standard): Payments are on time.

- SUB (Sub-Standard): Payments are overdue for 90+ days.

- LSS (Loss): The account is in default and unlikely to be recovered.

4. Not Addressing “Suit Filed” or Disputed Entries

Failing to act on negative remarks like “suit filed” can prolong the impact on your credit score.

5. Ignoring the Enquiry Section

Unchecked inquiries can hint at unauthorized attempts to access credit in your name.

Tips for Interpreting Your CIBIL Report Effectively

Reading your CIBIL report is not just about identifying your score but understanding the nuances that influence your financial health. Here are some tips for interpreting it effectively:

1. Focus on Repayment Trends

Examine your payment history to identify consistent patterns:

- Are EMIs and credit card dues paid on time?

- Are there any recurring late payments?

2. Understand How Each Section Impacts Your Score

- Credit Score: Reflects your overall creditworthiness.

- Account Information: Provides insights into your borrowing behavior and repayment capabilities.

- Enquiry Section: Highlights your credit-seeking behavior and its effect on your score.

3. Use Credit Simulators

Tools like CIBIL Score Calculators can help predict how changes in financial behavior (e.g., closing a loan or reducing credit utilization) will impact your score.

Also Read: CIBIL Score Calculation

4. Spot and Resolve Errors Quickly

- Discrepancies in repayment history or personal details can significantly impact your score.

- Raise a dispute with CIBIL immediately if errors are detected.

5. Regular Monitoring Is Key

- Check your CIBIL report at least once every three months to stay updated and address issues promptly.

- Use platforms that offer free credit report downloads to avoid unnecessary costs.

Conclusion

Your CIBIL report is more than just a document—it’s a gateway to understanding and improving your financial health. By learning to read and interpret your report effectively, you can:

- Monitor your creditworthiness.

- Spot and correct inaccuracies.

- Take actionable steps to enhance your credit score.

With this guide, you now have the tools to decode your CIBIL report confidently. Regular checks and disciplined financial habits will ensure your credit profile remains strong, opening doors to better financial opportunities.

Download the Buddy Loan app now!

Get the free Buddy Loan app on your phone

Having any queries? Do reach us at info@buddyloan.com

Frequently Asked Questions

Q. How to Read CIBIL score?

A. A CIBIL score ranges from 300 to 900; higher scores indicate better creditworthiness, with detailed credit history in the report.

Q. How can I access my CIBIL credit report online?

A. You can access your CIBIL report by visiting the CIBIL website, registering, and verifying your identity with PAN and other details.

Q. How do I interpret the CIBIL score on my report?

A. Scores above 750 are good, indicating low credit risk, while scores below 600 suggest higher risk and need for improvement.

Q. How frequently should I check my CIBIL report for updates?

A. Check your CIBIL report at least once every quarter to monitor accuracy and address discrepancies promptly.

Q. What factors affect my CIBIL score on the report?

A. Payment history, credit utilization, credit mix, credit inquiries, and credit history length are key factors.

Q. How long does it take to update my CIBIL report?

A. Updates typically take 30–45 days after lenders report changes to CIBIL.