There is an enormous impact of the foreclosure on your credit score and this would stay for a good 7 years. Enhancing the credit score instantly is the biggest benefit you have to make the best use of. It is a common misconception that foreclosure is more of evicting you from your house. This article helps you understand foreclosure and its impact on medical loan.

Get Personal Loan Online Up to ₹15 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

What is Loan Foreclosure?

The defined legal process by which the said lender takes control of a property may be mentioned under a mortgage, in the event of the borrower not being able to pay the full principal amount and interest payments is known as foreclosure or pre-closure.

The terms and conditions are stipulated in the mortgage contract. The foreclosure process takes its legal basis from a deed of trust contract, which is the mortgage contract, which gives the right to use a property owned by the borrower to the lender. This comes into effect when the borrower fails to uphold their repayment obligation.

A foreclosure is an actual act of a lender seizing a property cited under mortgage in the trust or mortgage contract. Essentially, foreclosure is the process of repayment of the outstanding personal loan in full in a single instalment. This mostly happens ahead of the due date.

Process of Foreclosure!

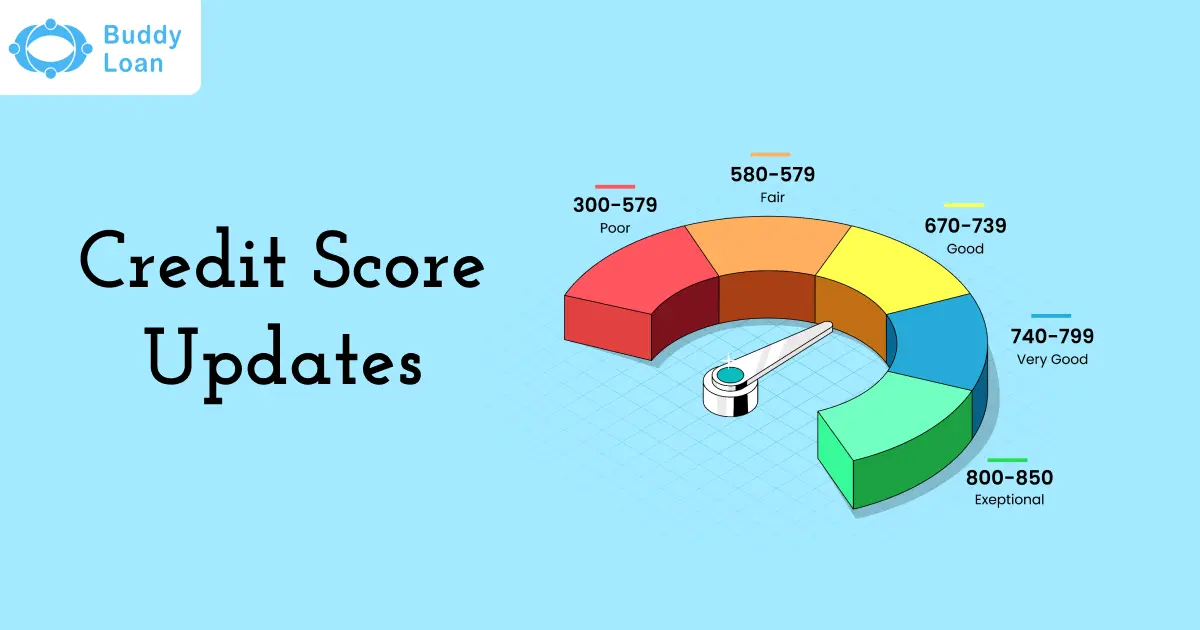

The foreclosure or pre-closure of a loan account can either be undertaken by the borrower or the lender. A medical loan is another type of personal loan, if you decide to foreclose or pre-closure the loan there is a direct hit on the credit score. The crude truth is that it will bring down your credit score.

The reasons for a lender foreclosing an account are pretty straightforward, but the reasons for a borrower doing the same are complex. Understanding those reasons may help an individual to get to a decision.

Common Reasons For Loan Account Foreclosure by a Borrower include the Following

- The need for a borrower to be debt-free

- Struggling with the pressure of paying monthly instalments with interest

- Deciding not being able to pay the upcoming instalment by any means

- Failing to pay subsequent instalments

- Hike in interest rates

The process of foreclosing an account by a borrower comes with some minor complications. The borrower first has to check with the lender and communicate that they want to foreclose the account and go through the appropriate terms and conditions.

Lenders, in most cases, allow a foreclosure, but the borrower may have to pay a foreclosure charge, in some cases. The usual range of the charge is 3%-6% of the principal amount that is yet to be paid.

After going through all these steps, the borrower can then demand a foreclosure.

Foreclosure or pre-closure is the process of repaying in full, the outstanding personal loan in one single instalment, ahead of the due date. A personal loan account (depending on the lender you avail it from), usually has a 1-year lock-in period, after which you have the option of prepaying the balance and settling the loan account. Read on to know how to foreclose a personal loan.

Get Personal Loan Online Up to ₹15 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

When the Bank Forecloses the Loan

Though this is one of the last resorts for a lender, it does become necessary when the borrower no longer remains financially capable to repay the loan amount and starts defaulting on EMI.

Getting an unsecured medical loan is easy via Buddy Loan. Your credit score takes shape from your repayment behaviour. If there are any defaults your credit score is bound to go low and if you clear the payments or EMIs on time, all the more good. To clear this confusion off the chart Buddy Loan presents better repayment options to help you enhance your credit score.

What the lender does is that it proceeds to auction the borrower’s collateral first, and then having raised the money equivalent to the outstanding amount, forecloses the loan account.

When the Borrower Forecloses the Loan

The reason why borrowers decide on foreclosing their loan account is the need to be debt-free. However, closing the account in haste, without checking with the lender on foreclosure terms and conditions, isn’t a wise decision. Here is a checklist that will hold you in good stead should you decide to foreclose the loan:

Does the lender allow foreclosure? Remember that not every lender will let you pre-close your account

Get Personal Loan Online Up to ₹15 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

What Are The Charges for Foreclosing

If your lender does allow a foreclosure, chances are that you may have to pay a foreclosure charge, which usually ranges from 3% to 6% of the principal amount that is yet to be paid.

Bajaj Finserv offers an instant Personal Loan where you can borrow up to Rs.25 lakh and foreclose the loan by paying a nominal foreclosure charge.

Read about the current personal loan fees and charges here.

Some Facts on Personal Loan Foreclosure:

Note the following facts before you make a decision of foreclosing your loan:

- Since maximum lenders wouldn’t allow a foreclosure within the first year of loan disbursal, borrowers get a raw deal when they realize a major portion of the interest is all that has been paid through the 12 months while the principal is still at large. So, the trick here is to prepay the amount as early as possible into the tenor, so as to avoid foregoing savings on the interest component.

- Remember to carry your identity proof, loan account number and a cheque for prepaying the balance loan when you approach the lender for a foreclosure.

Download the Buddy Loan App Now! One solution to each of your financial needs at your fingertip. Scan to download now

Having any queries? Do reach us at info@buddyloan.com