Credit scoring models determine the credit behavior of the consumer. This three-digit score is a measure of how you have managed your finances. Lenders use various credit scores to evaluate the risk when lending money. People often confuse FICO scores and Credit scores. However, there is a significant difference between FICO scores and credit scores regarding their work and what they mean. This 5 minute article is an attempt to sort out that confusion.

FICO creates scores for different products, and other companies also generate their own credit scores. A credit score is a general name that analyzes consumer credit reports to determine a score. Whereas, FICO provides a specific brand of credit score. It determines the creditworthiness of a consumer. But some lenders have their own credit scoring models or use competitors’ credit scores. Therefore, understanding the difference between FICO scores and credit scores and how they work is essential for maintaining excellent financial health.

Personal Loan

Quick Approval in 24 Hours

💰 No processing fee for first 100 customers | ⚡ Digital KYC in 5 minutes

What is a FICO Score?

While surfing the internet, you must have received information about credit scores. But have you ever heard of a FICO score?

The FICO score was developed by Fair Isaac Corporation and is a three-digit numeric representation of a customer’s value. It is generally generated by three bureaus (Equifax, Experian, TransUnion) for a diversified scoring system. The bureau’s credit report outlook is similar to that of a credit score, but the source of the evaluation is different.

Let’s examine what a FICO score consists of:

Credit reports are used to calculate FICO scores, and the calculations are based on the following five factors:

-

Customer’s Payment History:

FICO credit scores are based on your payment history, accounting for 35% of your total score. If you pay on time, you will see an increase in your score, but you will lose points if you pay late or miss a payment.

-

Customer’s Credit Utilisation:

The amount of credit utilised at any given time is called credit usage or credit utilization. Credit usage contributes 30% to your FICO score.

-

Customer’s Credit Life:

An individual’s credit age or life measures the average time they have used the credit. Generally, a person’s credit age should be higher than their credit life. FICO credit scores are calculated using this component to calculate 15% of the score.

-

Types of Credit Used by Customers:

FICO also considers a person’s credit, such as installment loans vs revolving credit. This credit mix accounts for 10% of FICO credit scores.

Credit inquiries made by the customer: Out of all, 10 percent of all the customer’s queries so far regarding loan or credit applications.

Lenders can use FICO credit ratings and other credit scores to forecast your ability and commitment to repay debt. It’s critical to think about maximizing your credit score, no matter which credit scoring algorithm is employed.

Also Read : What Does A Credit Score Mean, And What Factors Influence It

Is FICO Score Same as Credit Score?

Based on the credit risk score, a FICO score predicts if someone is likely to fall 90 days behind on a bill within the next 24 months. FICO uses complex algorithms to predict your score based on information in your credit report. FICO creates new versions of its scores to work with the database of each bureau’s databases, which is why there are many FICO Scores. Other companies also create credit scores that analyze consumers’ credit reports to generate scores. Hence, it indicates that FICO and credit scores are maybe similar but not the same.

What is the Difference Between FICO Score and Credit Score?

To dispel your doubts, let’s discuss a few differences between FICO score and credit score. Following is a table that summarizes FICO score vs credit score:

| FICO score | Credit score |

| FICO scores are a kind of credit score but follow a different scoring model proprietary developed by FICO standards of scoring. | A credit score is simply a measure of an individual’s creditworthiness based on his or her past credit history and ratings. |

| A FICO score is a three-digit value that ranges from 300 to 850, with 850 being the highest possible score. | Credit score represents an individual’s creditworthiness in three-digit numeric expressions ranging from 300 to 900. |

| FICO uses a unique and slightly complex algorithm based on the information available in the credit report from each of the national credit bureaus. | It uses a simple pattern generated in one’s credit report based on the credit ratings and transaction history. |

Personal Loan

Quick Approval in 24 Hours

💰 No processing fee for first 100 customers | ⚡ Digital KYC in 5 minutes

FICO Score Range

The table below shows the FICO score range:

| FICO SCORES | CREDIT RATINGS |

| 800 to 850 | Exceptional |

| 740 to 799 | Very Good |

| 670 to 739 | Good |

| 580 to 669 | Fair |

| 300 to 579 | Poor |

The above table shows that a score above 750 gives you high eligibility to avail of a personal loan at lower interest rates.

Why Is My FICO Score Different From My Credit Score?

As mentioned above, FICO generates different FICO Score models based on each credit bureau’s credit report. And it releases new FICO Score models per changing consumer behaviour, new regulations and technological advances. Moreover, it generates industry-specific scores for auto and credit card lenders. FICO gives creditors a more tailored score, which usually ranges from 250 to 900. This shows that not all lenders use the same scoring models or versions. Hence you may have different scores.

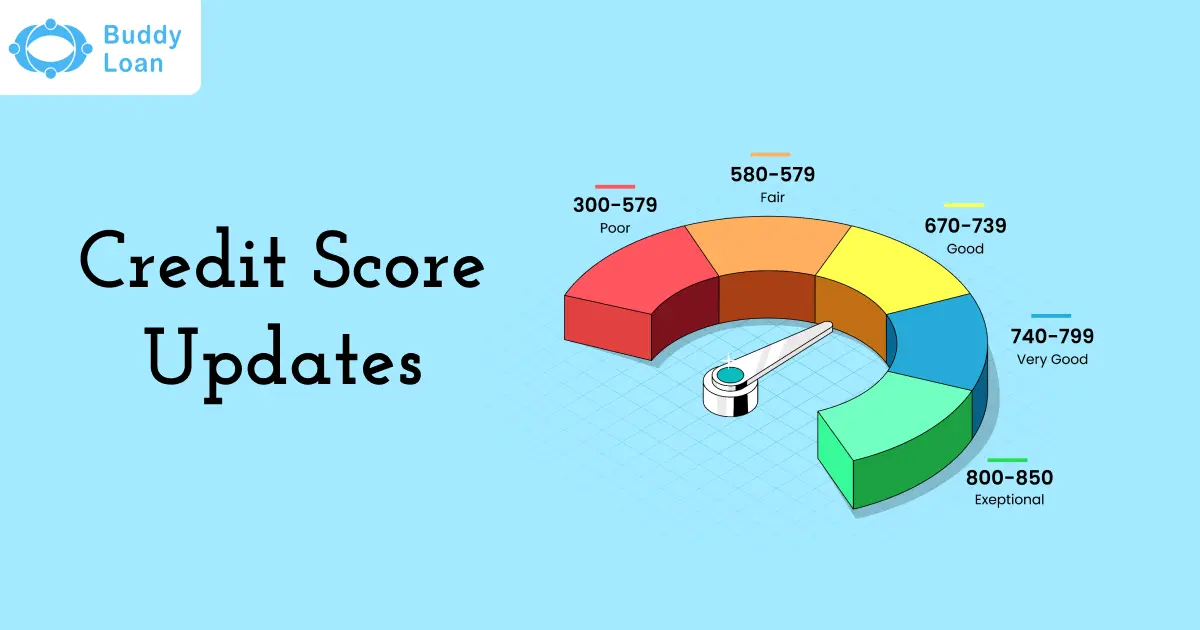

Credit Score Range

Although there are more than one credit score model available, most of the credit score range is similar to the following:

| Credit Score Range | Description |

| 800 to 850 | Excellent |

| 740 to 799 | Very good |

| 670 to 739 | Good |

| 580 to 669 | Fair |

| 300 to 579 | Poor |

-

800 to 850: Excellent

If you have a score in this range, you are considered to be a low-risk borrower. Moreover, you can quickly secure a loan with lower interest rates.

-

740 to 799: Very good

A score in this range demonstrates a history of good credit behaviour and may have a higher chance of your loan being approved for higher credit.

-

670 to 739: Good

This scoring range is considered good. However, lenders will view you only as an acceptable borrower. You may get approved for your loan, but there are less chances of getting a lower interest rate.

-

580 to 669: Fair

Lenders will consider you a “subprime” borrower if you score in this range. Lenders may perceive you as high-risk, so you may have trouble qualifying for new credit.

-

300 to 579: Poor

Applicants with a credit score in this range will have difficulty getting their loan approved. Hence, you will need to take measures to improve your credit scores before you can apply for any new credit.

What Are The Benefits of a Good Credit Score?

A good credit score is crucial when you want a low-interest personal loan or a new line of credit. We confront many circumstances in our day-to-day lives where we get rejected for a loan application, and it is only because of a poor or bad credit score in many cases. Your credit score significantly impacts the chances of getting a loan approved, as it is a measure that lenders use to gauge your ability to repay the loan within the set term.

However, if you want to save money and have a good credit score, here are a few suggestions: try to pay your bills on time, keep credit card balances low, keep old accounts open, use multiple forms of credit, and limit your borrowing. A good credit score also allows you to save more. The higher your credit score, the easier it will be to obtain approval for low-interest loans. However, managing your credit and lines responsibly is always suggested to build a healthy and lucrative score for the future.

Also Read : What Is A Credit Score And What Is It Used For

Factors that Affect Your Credit Score

Your credit score depends on various factors, namely:

Payment History:

It significantly influences your credit score, which indicates your creditworthiness. Hence, if you miss out on your payments, it will drastically affect your credit score. Lenders will also check your payment history to make sure you can repay on time when approving your loan application.

Credit Utilization Ratio (CUR):

The credit utilization ratio is the amount payable with your credit limit. If you utilize your credit beyond the maximum credit limit, you will be seen as credit hungry; hence, your score will drop. Moreover, lenders will doubt your ability to repay your loan as you depend more on credit for spending. Therefore, maintain your credit utilization ratio to less than 30% of your income.

The Number of Credit Inquiries:

There are two types of credit inquiries- Soft Inquiries and Hard inquiries. Soft inquiries will not harm your credit score, whereas multiple hard questions will decrease your credit score. When you apply for a loan from various lenders, each lender will conduct a credit check to evaluate your credit score, which records as a hard inquiry in your credit report reducing your score.

Length of Credit History:

A long credit history indicates good credit behaviour. It means that you have maintained and repaid your dues on time consistently. Therefore, your credit score will also be good when you have a long credit history.

Credit Mix:

Have a diverse credit mix, such as student loans, car loans, and credit cards, to increase your credit score. It shows how well you can manage a variety of credits.

Personal Loan

Quick Approval in 24 Hours

💰 No processing fee for first 100 customers | ⚡ Digital KYC in 5 minutes

Take These Steps To Increase Your Credit Score

Let us look at the top 10 strategies to improve your credit score:

Check Your Credit Report

Your credit report may have errors when your transactions need to be updated in your account. It is suggested to regularly check your credit report once a year to identify any potential errors. It will also help you know more about your financial health, payment status, and errors. If you identify any errors in your report, raise the dispute immediately with the respective credit bureau. Once the mistake is rectified, you will significantly improve your credit score.

Make Corrections To Errors

Leaving your errors unchecked can drastically affect your score, as it will reflect in your credit for at least seven years. If you find any error, raise the dispute immediately and get it rectified within 30 days.

Credit Utilization Ratio (CUR)

Utilizing your credit card for all expenses indicates that you depend on credit. And if it crosses the maximum credit limit, your score will be reduced as it is considered credit-hungry behaviour. Therefore, avoid using your credit card for all transactions and maintain your credit utilization ratio to 30% or less. Doing so will help improve your credit score.

Don’t Apply For Credit If Rejected

When a lender does not approve your loan application, the information gets recorded in your credit report affecting your score. Despite that, they will check your credit score if you apply for a loan with another lender. And when your score is low, they will not approve your loan. Therefore it is suggested to improve your credit score before you apply for a loan again.

Pay Your Loans

If you have any missed out payments or pending dues, clear them as soon as possible. You can set reminders to repay your loan on time. And if you are still facing issues with loan repayment, you can talk to your lender and restructure your debt repayment. This will help you repay your loans quickly.

Have a Balance

There are two types of loans-secured and unsecured. Having a credit mix, such as car loans, gold loans, personal loans, etc., shows that you are good at managing your debts. Therefore, maintain a balance of both secured and unsecured loans to show that you can repay both types of loans.

Keep Your Old Credit Accounts Open

Old credit accounts have a longer credit history. And this will indicate that you have been consistent in your repayments and will increase your creditworthiness. Therefore, do not close your old account even if you no longer use them to improve your score.

Borrow Minimum

Avail of a loan amount for only what you require. If you avail of more than your need, you will face difficulties repaying your loan on time. This will, in turn, reduce your credit score. Therefore, plan your budget and requirements before applying for a loan.

Watch Out For Joint Applicants

You may apply for a loan using a joint applicant when you have a poor score. And if the joint applicant cannot repay the loan on time, it will also damage his credit score. This way, you will have to suffer even if it’s not your fault. Therefore, choose a joint applicant wisely.

Wrapping Up

Understanding the difference between FICO score and credit score is essential to solving financial problems like borrowing money or taking out credit cards. A good credit score will also help you enhance your worth as a borrower or customer concerned about your credit rating and specific transactions. In this regard, Buddy loan takes care of your financial urges and finds you a solution in no time.

Download Personal Loan App

Get a loan instantly! Best Personal Loan App for your needs!!

Looking for an instant loan? Buddy Loan helps you get an instant loan from the best verified lenders. Download the Buddy Loan App from the Play Store or App Store and apply for a loan now!

Download the Buddy Loan app now!

Get the free Buddy Loan app on your phone

Having any queries? Do reach us at info@buddyloan.com

People Also Ask

Q. What Is The FICO Score?

A. The FICO score was developed by Fair Isaac Corporation and is a three-digit numeric representation of a customer’s value. It is generally generated by three bureaus (Equifax, Experian, TransUnion) for a diversified scoring system. The bureau’s credit report outlook is similar to that of a credit score, but the source of the evaluation is different.

Q. How Can You Improve Your FICO Score?

A. You can boost your FICO score by paying your bills on time, keeping your credit card balances low, and paying off your debt.

Q. Which Is Better Among FICO Scores And Credit Scores?

A. FICO credit scores may or may not be better than other credit scores based on how the scores are created and used. FICO scores consider multiple factors, including payment history, credit use, credit age, credit mix, and credit inquiries, which help lenders determine the likelihood of you repaying a loan.

Q. Are Credit Reports And Credit Scores The Same?

A. A credit score is a numerical measurement of one’s credit rating, which is determined by the individual’s credit history and typically ranges between 300 and 900. A credit report is a compilation of information that reflects an individual’s financial health and can be viewed digitally.

Q. What Is The Standard Credit Score?

A. A standard credit score could be defined as a credit score between 700 and 900, which can help you get various offers, including easy loan approvals with lower interest rates.

Q. Do Lenders Use FICO Scores or Credit Scores?

A. Almost 90% of lenders use FICO scores to determine your creditworthiness when approving your loan.

Q. Which Credit Bureaus Use FICO?

A. FICO score is generated by three bureaus (Equifax, Experian, TransUnion) for a diversified scoring system.