Your CIBIL score is a three-digit number that represents your creditworthiness. It ranges from 300 to 900, and a higher score increases your chances of getting approved for loans and credit cards at favorable interest rates. Many people struggle with low credit scores but don’t worry – improving your CIBIL score is entirely possible. In this blog, we will provide practical CIBIL score improvement tips to help you go from 600 to 750 or higher.

| Credit Score is a general term for a numerical representation of a person’s creditworthiness. CIBIL Score is a specific credit score from the Credit Information Bureau (India) Limited (CIBIL). |

More About Good CIBIL Score

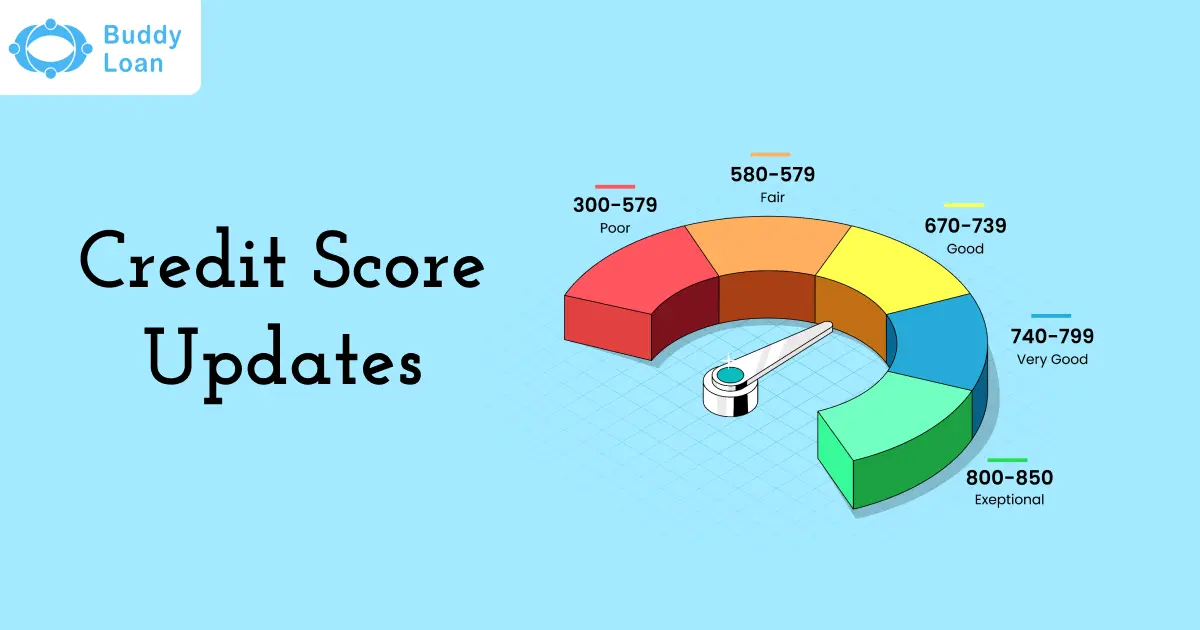

A good CIBIL score typically falls between 700 to 900. Here’s a breakdown:

| Score Range | Credit Status | Loan Approval Chances |

| 750 – 900 | Excellent | Very high chance of approval |

| 700 – 749 | Good | High chance of approval |

| 650 – 699 | Average | Moderate chance; may need higher interest |

| 600 – 649 | Poor | Low chance of approval |

| Below 600 | Very Poor | Very unlikely to be approved |

Importance of Good CIBIL Score

Understanding the importance of a good CIBIL score is crucial for anyone looking to achieve financial success and stability.

1. Loan Approval: Banks prefer giving loans to individuals with a high credit score.

2. Lower Interest Rates: A good score helps you get loans at better rates.

3. Credit Card Eligibility: Premium credit cards with high rewards are accessible with a good score.

4. Financial Stability: It reflects your responsible financial behavior.

5. Quick Approvals: Faster approval for loans and credit cards.

Top CIBIL Score Improvement Tips

CIBIL score improvement tips is easy with the right steps. Here are some simple tips to help you boost your credit score. Here are CIBIL score improvement tips:

1. Pay Bills On Time

Your CIBIL score acts as your financial report card, showing lenders how reliable you are with repayments. Paying your bills on time is one of the simplest and most effective ways to maintain or improve your score. A high CIBIL score can unlock benefits like better loan offers, lower interest rates, and access to premium credit cards.

Payment History Matters

Your payment history makes up around 35% of your total CIBIL score. It reflects whether you’ve paid your credit card bills, EMIs, and loans on time. Late or missed payments can damage your score and stay on your credit report for up to 7 years.

Example:

If your credit card bill is due on the 10th of the month, paying it on or before the 9th helps keep your CIBIL score high. A payment made after the 10th can negatively impact your score.

By making timely payments a habit, you not only protect your credit score but also enjoy smoother financial transactions and better credit opportunities.

2. Check Your CIBIL Report for Errors

Your CIBIL report is like a detailed record of your financial history. It contains information about your loans, credit card usage, repayments, and even personal details. Sometimes, errors can creep into your report, and these mistakes can lower your credit score even if you’ve managed your finances well. Correcting these errors promptly is essential to maintain a healthy credit score.

Common Errors in Your CIBIL Report

Here are some common mistakes you might find in your CIBIL report:

- Incorrect Personal Information:

Errors in your name, date of birth, or contact details. - Wrong Account Details:

Information related to your loan or credit card accounts that doesn’t match your actual history. - Mismatched Amounts:

Showing overdue amounts even when you’ve already paid off the debt. - Duplicate Accounts:

The same account listed more than once, creating confusion and affecting your credit history. - Incorrect Days Past Due (DPD):

Showing that you missed payments when you actually paid on time.

Example:

Let’s say you closed a loan after repaying the full amount. However, due to a clerical mistake, the report still shows the loan as overdue. This incorrect information can lower your credit score and make it harder for you to get future loans or credit cards.

3. Avoid Multiple Credit Applications in a Short Time

Applying for multiple loans or credit cards in a short period can harm your CIBIL score. Every time a lender checks your credit report before approving a loan or card, it creates a hard inquiry. Too many hard inquiries within a short time can make lenders cautious about approving your credit requests.

Reasons

- Signals Financial Stress:

When you apply for several loans or credit cards quickly, it can seem like you are facing financial difficulties and urgently need money. This raises concerns for lenders. - Increased Risk Perception:

Lenders may consider you a high-risk borrower if you apply for credit frequently. This can lead to loan rejections or higher interest rates if approved.

Example:

Imagine you apply for three credit cards in a single month. Each lender performs a hard inquiry on your credit report. This can reduce your credit score and make it harder for you to get approved for future loans or credit cards. Lenders might interpret this behavior as a sign of financial trouble.

4. Keep Your Credit Utilization Ratio Low

The Credit Utilization Ratio measures how much of your available credit you are currently using. It shows lenders how reliant you are on credit and significantly determines your CIBIL score.

Way It Works

- The ratio is expressed as a percentage.

- It is calculated by dividing the total credit balance (the amount you owe) by the total credit limit (the maximum amount you can borrow).

| Formula:

Credit Utilization Ratio = (Total Credit Used/Total Credit Limit) × 100 Example Calculation: Suppose you have two credit cards: Card 1: Credit limit of ₹50,000 with a balance of ₹10,000 Total Credit Limit: ₹50,000 + ₹30,000 = ₹80,000 Credit Utilization Ratio = (₹15,000 / ₹80,000) × 100 = 18.75% |

5. Consider a Secured Credit Card

Getting approved for an unsecured credit card can be challenging if you’ve faced financial setbacks and have a low credit score. In such cases, a secured credit card can be an excellent solution to rebuild your credit.

- To get a secured credit card, you need to provide a cash deposit as collateral.

- For example, if you deposit ₹10,000, your credit limit might be ₹5,000 or even the full deposit amount, depending on the bank’s policy.

Example:

- Deposit Amount: ₹10,000

- Credit Limit: ₹5,000

- Use the card for small purchases and ensure you pay the full balance each month to build a positive credit history.

6. Stay Informed About Co-signed or Guaranteed Loans

When you co-sign or guarantee a loan for someone, you share the responsibility for that loan. This means your credit score and financial health can be affected by the borrower’s actions. Here’s why it’s important and how to protect yourself.

Reasons

1. Affects Your Credit Score:

If the borrower misses payments or defaults, it will appear on your credit report and hurt your credit score.

2. Financial Responsibility:

As a co-signer or guarantor, you’re legally responsible for the loan. If the borrower doesn’t pay, you must step in to cover the repayments.

3. Debt-to-Income Ratio:

The loan you co-sign adds to your debt obligations, potentially affecting your eligibility for future loans or credit cards.

7. Don’t Close Old Credit Card Accounts

You might think closing an unused credit card is a good idea, but keeping old accounts open can actually help your credit score. Here’s why:

Reasons:

1. Longer Credit History:

Your credit score benefits from a longer credit history. By keeping your oldest credit cards open, you maintain a longer average account age, which positively impacts your score.

2. Lower Credit Utilization Ratio:

Closing a credit card reduces your overall credit limit. This can increase your credit utilization ratio (how much credit you’re using compared to what’s available), which may lower your credit score. A lower utilization ratio (ideally under 30%) is better for your score.

Example:

If you have two credit cards:

- Card 1: Credit limit of ₹50,000 (opened 5 years ago)

- Card 2: Credit limit of ₹20,000 (opened 1 year ago)

Close Card 1, your total credit limit drops from ₹70,000 to ₹20,000. If you have an outstanding balance of ₹10,000, your utilization ratio jumps from 14% (₹10,000/₹70,000) to 50% (₹10,000/₹20,000), which can hurt your score.

| A CIBIL report is a summary of your credit history and behavior. It includes your personal details, loan information, overdraft facilities, and your CIBIL score. |

Personal Loan

Quick Approval in 24 Hours

💰 No processing fee for first 100 customers | ⚡ Digital KYC in 5 minutes

Steps To Check Your CIBIL Score

1. Visit a Trusted Website or App:

Many financial platforms offer free CIBIL score checks. Some popular options are:

- Buddy Loan: A digital Fintech Loan marketplace

- CRED: A rewards app for credit card users.

- Paisabazaar: A financial services marketplace.

- Bank Websites: Some banks provide free CIBIL score checks for their customers.

2. Enter Your Details:

You’ll need to provide basic information like:

- PAN Card Number (your unique taxpayer ID)

- Date of Birth

- Mobile Number (for OTP verification)

3. Verify Your Identity:

Complete the verification process, which may involve:

- OTP Verification: Enter the OTP sent to your mobile number.

- Aadhaar Linkage: Sometimes, linking your PAN with Aadhaar is required.

4. Check Your CIBIL Score:

Once verified, you’ll see your CIBIL score (ranging from 300 to 900). A score above 750 is considered good.

Factors That Impact Your CIBIL Score

1. Payment History:- Making timely payments on loans, credit cards, and EMIs shows lenders that you are reliable. Late or missed payments can significantly damage your score and affect your creditworthiness.

2. Credit Utilization:- Using more than 30% of your total credit limit indicates over-reliance on credit. Keeping your credit usage low helps maintain a healthy score and shows you are managing your credit responsibly.

3. Length of Credit History:- A longer credit history gives lenders a better picture of your borrowing behavior. Keeping older credit accounts open can help improve your score over time.

4. Credit Mix:- Having a balanced mix of secured loans (like home loans or car loans) and unsecured loans (like credit cards) demonstrates your ability to manage different types of credit, boosting your score.

5. New Credit Inquiries:- Applying for multiple loans or credit cards within a short period can signal financial stress. Each hard inquiry made by lenders can lower your score temporarily, so space out your applications.

Conclusion

CIBIL score improvement tips is a gradual process, but with consistent effort, it can be done. By paying bills on time, maintaining low credit utilization, and checking your credit report regularly, you can easily boost your score from 600 to 750. A good CIBIL score opens doors to better financial opportunities, including loan approvals, lower interest rates, and premium credit cards. Follow these CIBIL score improvement tips and take charge of your financial future today!

Download Personal Loan App

Get a loan instantly! Best Personal Loan App for your needs!!

Looking for an instant loan? Buddy Loan helps you get an instant loan from the best verified lenders. Download the Buddy Loan App from the Play Store or App Store and apply for a loan now!

Get the free Buddy Loan app on your phoneDownload the Buddy Loan app now!

Having any queries? Do reach us at info@buddyloan.com

Frequently Asked Questions

Q. What is a good CIBIL score?

A. CIBIL score above 750 is considered good, increasing your chances of loan or credit card approval with favorable terms.

Q. How can I improve my CIBIL score quickly?

A. Pay bills on time, reduce outstanding debts, maintain a credit utilization ratio below 30%, and avoid multiple loan applications.

Q. Does checking my CIBIL score frequently affect it?

A. No, checking your score yourself is a “soft inquiry” and does not impact your credit score.

Q. Can closing a credit card affect my CIBIL score?

A. Yes, it can lower your score by increasing your credit utilization ratio or shortening your credit history length.

Q. How does my credit utilization ratio affect my score?

A. High utilization ratio (above 30%) signals dependency on credit and can reduce your score, so maintaining a low ratio is crucial.

Q. What should I do if I find an error in my credit report?

A. Report the discrepancy to CIBIL or your lender immediately to rectify it and ensure it doesn’t impact your score.

Q. Does having a mix of credit types affect my score?

A. Yes, a healthy mix of secured and unsecured loans positively impacts your score by showing diverse credit management.

Q. How long does it take to see an improvement in my score?

A. Improvement can take 3–6 months or longer, depending on your financial discipline and credit history corrections