TransUnion CIBIL Ltd. formerly known as Credit Information Bureau Ltd. is one of the leading Credit Information Companies in India. It was incorporated in 2000 and is popularly known as CIBIL credit bureau. The credit bureau collects and maintains records of all your payments related to various credit products such as loans and credit cards. Lenders and financials submit your credit records to CIBIL on monthly basis. The Bureau then uses this information and generates your Improve your CIBIL score along with a detailed credit report. And when you apply for a loan, lenders will use this report and credit score to determine your creditworthiness and know whether you can repay the borrowed amount.

Moreover, lenders expect you to have a score of above 750. And if you have a low credit score, your chances of getting your loan approved will reduce. Therefore, you have to take measures to improve your credit score to increase your chances of getting a loan.

So if you are having a low score, read this article further to know more about CIBIL score and strategies to improve it.

What is a CIBIL Score?

A CIBIL score is a 3-digit numerical representation of your creditworthiness. It usually ranges from 300-900. Having a high credit score shows that you have been a responsible borrower and have a good credit history. It also shows that you can repay your loan on time without defaulting. Moreover, having a score above 750 will increase your chances of getting your loan at comparatively low-interest rates.

Factors that Affect Your CIBIL Score

Your CIBIL Score depends on various factors namely:

Payment history:

It is one of the essential parts of your credit score. So if you miss out on your payments or delay your expenses, it will affect your credit score. Moreover, lenders will check your payment history to make sure that you have the ability can on time when approving your loan application.

Credit utilization Ratio:

The credit utilization ratio is the ratio of the amount payable with that of your credit limit. So if you use your credit beyond the maximum credit limit, your credit score will drop. As a result, lenders will doubt your ability to repay your loan amount on time. Hence, maintain your credit utilization ratio to below 30% of your income.

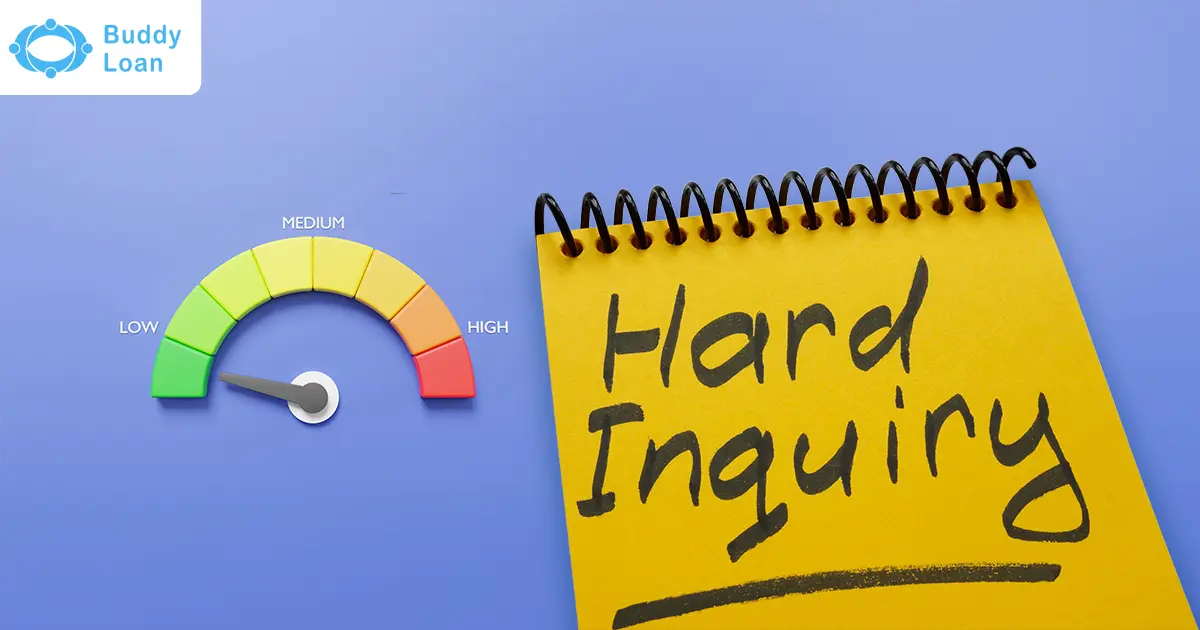

The Number of Credit Inquiries:

Credit inquiries are of 2 types: Soft Inquiries and Hard inquiries. Soft inquiries do not harm your score whereas multiple hard credit inquiries will harm your credit score. Because when you apply for loans from multiple lenders at a time, each lender will check your credit score which creates a hard inquiry resulting in a drop in your score.

Length of Credit History:

Lenders usually notice the length of your credit history to know your credit behavior. And your credit score will be good if you have a long credit history.

Credit Mix:

Having a diverse credit mix likewise student loans, car loans, and credit cards increase your credit score. The reason is that it shows how well you can manage a variety of credits.

Also Read: 10 Essential Habits for a High Credit Score

Role of CIBIL Score in Loan Approval

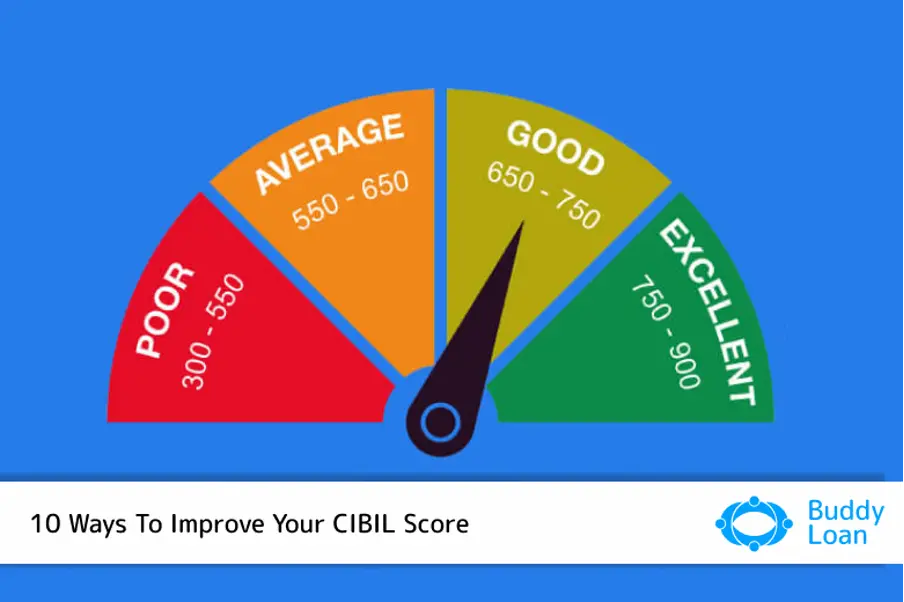

Your CIBIL score plays a vital role in your loan application process. It helps banks and financial institutions to determine your creditworthiness and use it to make a lending decision. And generally, you must have a score of above 750 to qualify for a loan. So below are the different ranges of a CIBIL score.

| CIBIL score range | What does it mean for your credit health? |

| 300-549 |

|

| 550-649 |

|

| 650-749 |

|

| 750-900 |

|

Also Read: Want to Achieve a Good CIBIL Score? Here are some practical tips

Get Personal Loan Online Up to ₹15 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Myths About CIBIL/Credit Score

Here are some of the most common myths associated with CIBIL score:

1. CIBIL score does not impact your loan eligibility

Since the CIBIL score represents your creditworthiness, having a high CIBIL score will make you a low-risk borrower and increase the chances of your loan approval. Apart from enhancing your loan eligibility, a high credit score will also qualify you for a higher loan amount at a lower interest rate. Therefore, your CIBIL score has a significant impact on your loan eligibility.

2. Making investments can harm your CIBIL score

Making smart investments will help you secure your future without hurting your CIBIL score. However, if you delay your EMI payment, it can have a negative impact on your CIBIL score significantly. Therefore, making investing will solely not affect your CIBIL score.

3. You cannot get a loan with a low credit score

Getting a loan can be challenging if you have a low CIBIL score. However, there are lenders who may still approve your loan application even if you have a low CIBIL score. It is to be noted that lenders may charge you a high-interest rate while offering personal loans with low CIBIL scores. Therefore, you can still get a loan with a low credit score.

Precautionary Measures To Maintain a Good CIBIL Score

A low CIBIL score can be a huge hindrance especially when you are in need of instant loans as lenders will consider you a high-risk applicant. So in order to avoid getting into such a hectic situation, it is important to take precautionary measures to maintain a good credit score. So here are steps you can take to do so:

1. Check your current CIBIL Score:

First check your current CIBIL score to know if any rectification is needed. You can send a Credit Information request on the official website of CIBIL. Just submit the required documents and pay ₹470 on the website after which the authentication process will take place. Once the authentication is complete, you will get your CIBIL score through your registered email ID.

2. Check your details in the Credit Report:

Once you get your credit score, check if all your details such as your bank account, loan details, credit card details, your identity, the status of your account, etc are accurate.

3. Know where you went wrong:

It is essential to know how to read your credit report so that you find where and why your score has been reduced.

4. Identify potential errors in your credit report:

Sometimes errors can occur when your bank or financial institution gives information to CIBIL. Such errors in your credit report can lower your score. So if you identify any error, you have to raise a dispute to CIBIL by sending a request form. Errors can occur in Account balances, Overdue loan amounts after repayment, Identity theft, and details of a loan that you have not availed.

5. Be open to changing your Credit Behaviour:

Once you identify the exact reason why you have a low credit score and the errors, you have to take constructive steps to improve your score. Find ways to clear all your unpaid and outstanding debts.

6. Speak to your lenders:

If you are confused about how to improve your score, you can talk to your lenders to build strategies to increase your credit score and clear your debts.

7. Maintain your score above 750:

Once you have successfully increased your credit score above 750, you have to keep the balances low on your credit cards, make loan repayments on time and maintain diverse credit products like secured and unsecured loans.

Get Personal Loan Online Up to ₹15 Lakhs

By entering your number, you're agreeing to Terms & Conditions & Privacy Policy.

Reasons Why Your CIBIL Score Is Low

Many times your CIBIL score drop because of your past behavior. Some of the common errors that you might be making:

Outstanding Credit Card Balance: If you do not pay your total credit card bills every month and only pay the minimum amount due, it will leave an outstanding balance on your credit cards. As a result, it will reduce their CIBIL score.

Too Many Loans or Credit Cards – If you apply for too many loans or credit cards, then every time a lender checks the credit report or credit score to process the loan or credit card application it is recorded as a hard inquiry. And multiple hard inquiries will result in a reduction in your CIBIL score.

High credit usage – If you use more than 30% of your credit limit, then it will have negative effects on your score as it shows that your dependency on credit is high.

Delay in repayments – If you delay in making your EMI payments, then it will be recorded in your CIBIL report, which will further reduce your credit score.

Also Read: Solutions For Your CIBIL Credit Report Issues

Strategies To Increase your CIBIL Score

Now that we know what is a CIBIL score, let us look at the top 10 strategies for CIBIL score improvement tips:

Check Your Credit Report

You have to check your credit report frequently as it will help you know more about your financial health, payment status, and potential errors. If you find any errors in your report, raise the dispute with CIBIL immediately. Once it gets rectified, your score will also improve.

Also Read: In How Many Days CIBIL Score is Updated

Make Corrections to Errors

If you find any error, you can raise the dispute immediately by visiting the official website, www.CIBIL.com. Moreover, you have to raise the disputes within 30 days and rectify the same.

Credit Utilization Ratio

You have to avoid using your credit card for all transactions. Therefore, maintain your credit utilization ratio at 30% or less. When you do this, you will see a positive effect on your CIBIL score.

Don’t keep applying for credit if rejected

If your loan application gets rejected, the information will be recorded in your credit report. Despite the rejection, if you again apply for a loan with another lender, they will know your low credit score and the previous rejection and might not approve your loan. Therefore it is best to improve your credit score first before you apply for a loan again.

Keep the frequency of applications low

Avoid applying for loans from multiple lenders. The reason is that each time you apply for a loan, lenders will perform a credit check to determine your credit score. This will record in your credit report as a Hard inquiry. And if there are multiple hard inquiries, it will negatively affect your credit score and will make look credit hungry.

Pay your loans

If you have any pending loans or missed out payments, start paying as soon as possible. And is you are facing any struggle with your current loan repayment, you can talk with your lender to restructure your debt to make repayment easier.

Have a balance

There are two types of loans namely secured and unsecured. If you avail of too many unsecured loans, lenders will see it as negative financial behavior and might reject your loans. Therefore, maintain a balance of both secured and unsecured loans as this will indicate that you can manage both types of loans.

Keep your old Credit Accounts open

Do not close your old account that has been paid off, even if you don’t use them any longer. This is because keeping the old account open will increase the length of your credit history which will in turn improve your credit score.

Borrow Minimum

Do not borrow a loan amount more than you require. The reason is that you will have difficulties in repaying your loan amount on time which will affect your credit score. Therefore, plan and budget your requirement and borrow the loan amount only for what you need.

Watch out for joint applicants

Sometimes you might suffer even if it’s not your fault if you have a joint applicant. This is because if the joint applicant is not able to repay the loan amount and defaults on it, it will affect your credit score as well.

Final Note

Hope this article would have given you a detailed picture of your CIBIL score and the strategies to improve your CIBIL score. Having good financial practice will not only help you increase your score but will also increase your credibility.

Download Personal Loan App

Get a loan instantly! Best Personal Loan App for your needs!!

Looking for an instant loan? Buddy Loan helps you get an instant loan from the best verified lenders. Download the Buddy Loan App from the Play Store or App Store and apply for a loan now!

Download the Buddy Loan App Now! One solution to each of your financial needs at your fingertip. Scan to download now

Having any queries? Do reach us at info@buddyloan.com